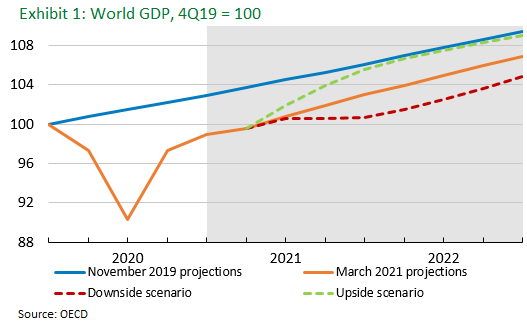

The improved outlook in the U.S. has led to upward revisions of 2021 global growth. The OECD lifted its World Real GDP forecast by 1.4 percentage points to 5.6% in early March, which followed the IMF’s 0.3 percentage point upward revision in January to 5.5%. Market estimates have also centered around this level. Risks have become more asymmetric to the upside with additional U.S. fiscal stimulus and closer proximity to herd immunity in the developed world. In an optimistic scenario, this could result in World GDP recovering to its pre-COVID path this year, according to the OECD March interim outlook (Exhibit 1).

The improved outlook in the U.S. has led to upward revisions of 2021 global growth. The OECD lifted its World Real GDP forecast by 1.4 percentage points to 5.6% in early March, which followed the IMF’s 0.3 percentage point upward revision in January to 5.5%. Market estimates have also centered around this level. Risks have become more asymmetric to the upside with additional U.S. fiscal stimulus and closer proximity to herd immunity in the developed world. In an optimistic scenario, this could result in World GDP recovering to its pre-COVID path this year, according to the OECD March interim outlook (Exhibit 1).

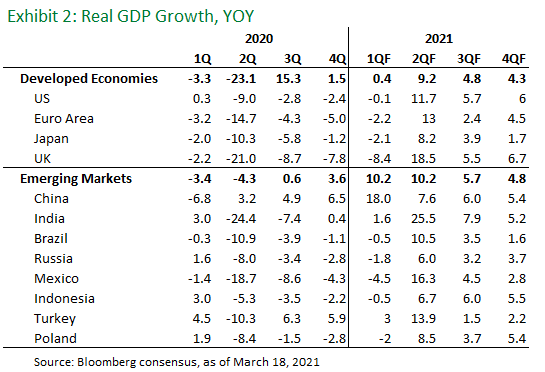

In EM, we continue to expect the degree of recovery to vary significantly on virus and vaccine management, economic openness particularly in the U.S., and the ability to effectively recalibrate macroeconomic policy amid evolving external growth and financial conditions. Chinese data should improve moderately in the coming month on looser restrictions but gradual policy normalization will likely result in easing sequential growth as the year progresses, potentially posing modest headwinds to 2Q consensus (Exhibit 2).

There have been a few early leaders in EM vaccine rollout including Israel, Bahrain, Chile, and Morocco while Malaysia, Mexico, India, Brazil, Colombia, the Dominican Republic and Argentina have procured enough vaccine for 70% of their populations. Sustained elevated commodity prices and improved global demand should continue to provide a boon for open export oriented economies while performance of more domestic and service led countries will rely on local health conditions and travel guidelines. Select tourism markets should begin to see more meaningful green shoots.

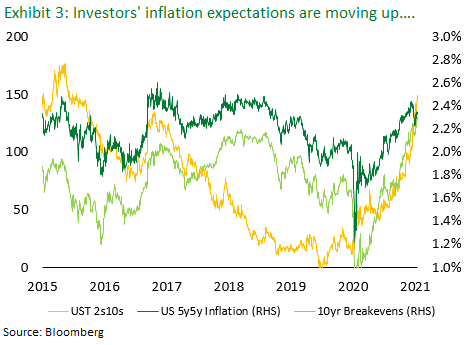

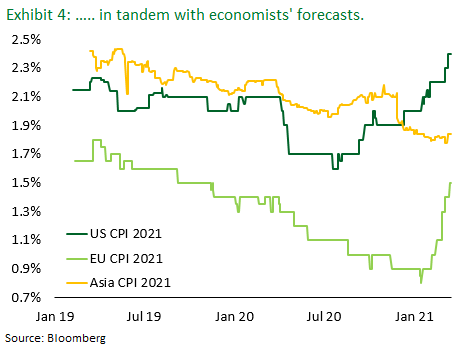

The improving fundamental backdrop and projected strong economic rebound in 2021, especially in the U.S. on the back of the extraordinarily large fiscal stimulus delivered by the Biden Administration, have shifted market inflation expectations materially higher, albeit from a low base. Early 2Q is likely to offer the first real test for investors’ tolerance of higher inflation relative to the recent past as PCE inflation is expected to rise above 2% given base effects from a year ago.

The improving fundamental backdrop and projected strong economic rebound in 2021, especially in the U.S. on the back of the extraordinarily large fiscal stimulus delivered by the Biden Administration, have shifted market inflation expectations materially higher, albeit from a low base. Early 2Q is likely to offer the first real test for investors’ tolerance of higher inflation relative to the recent past as PCE inflation is expected to rise above 2% given base effects from a year ago.

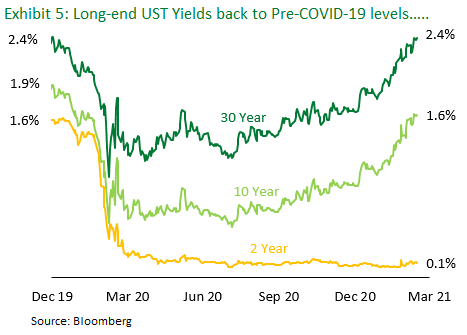

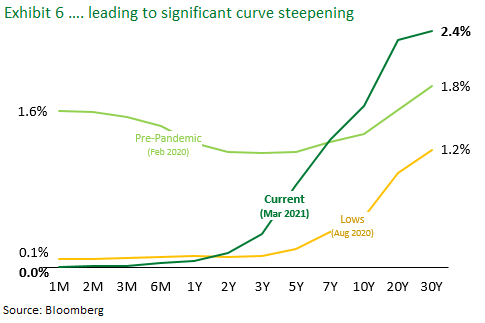

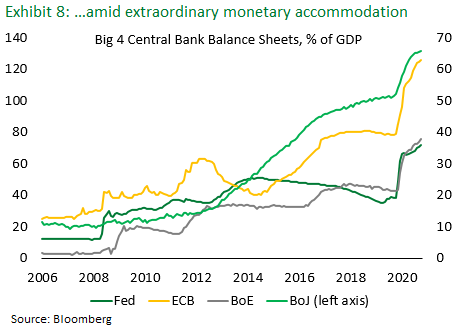

Concerned by the prospect that inflation overshoots could force the Fed to tighten monetary policy and start to taper asset purchases much sooner than it has been signaling, investors have propelled U.S. bond yields higher and steeper, creating significant pressure on EM assets, especially longer duration ones with limited spread cushion. Thus far, the Fed has remained unperturbed by the rapid repricing of inflation expectations and UST yields. Chairman Powell has clearly indicated that in the FOMC’s view, a potential spike in inflation during 2Q is likely to be “transitory” and that evidence of “substantial further progress” on employment and inflation is required before the Fed considers starting to taper policy accommodation.

2Q is likely to be “transitory” and that evidence of “substantial further progress” on employment and inflation is required before the Fed considers starting to taper policy accommodation.

Within its new “average inflation targeting” framework and after years of failing to reach its 2% target, the Fed appears committed and willing to accept above-target inflation in the U.S. economy for a period of time, especially if that would support a more equitable recovery in the labor market. However, there is a reasonably high probability in our view that markets continue to push UST yields higher as 2Q progresses. In such a scenario, we expect this to motivate an eventual intervention by the Fed. Chairman Powell has made it clear he will not tolerate market-destabilizing volatility or a persistent tightening  of financial conditions that could put the achievement of the Fed’s objectives at risk. We think that extending the weighted average maturities of current holdings from 64 months, i.e. Operation Twist 3.0 is the most likely tool for targeting long-end rates, while more explicit yield curve control is also an option for the Fed.

of financial conditions that could put the achievement of the Fed’s objectives at risk. We think that extending the weighted average maturities of current holdings from 64 months, i.e. Operation Twist 3.0 is the most likely tool for targeting long-end rates, while more explicit yield curve control is also an option for the Fed.

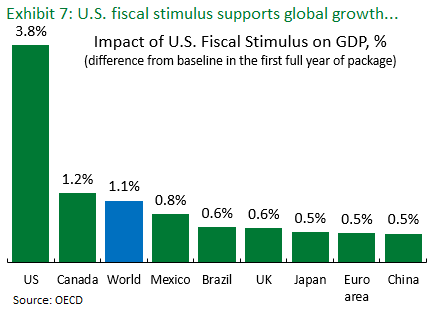

Market concerns about faster than expected reflation and higher UST yields notwithstanding, extraordinary fiscal stimulus by the Biden Administration in 2021-22 will also provide a substantial boost to global growth vs. the baseline, all else being equal. This will support the cyclical recovery across EM, albeit to various degrees. In addition to highly stimulative fiscal policy in developed markets (“DM”), we also expect the systemic CBs to remain flexible, patient and react only to sustained higher (average) inflation. Against this backdrop, we do not anticipate global financial conditions to tighten to a level that challenges the global recovery in the near term, but select EM economies more vulnerable to outflows may face greater pressure to adjust policy more swiftly, potentially shortening their cyclical rebound.

Market concerns about faster than expected reflation and higher UST yields notwithstanding, extraordinary fiscal stimulus by the Biden Administration in 2021-22 will also provide a substantial boost to global growth vs. the baseline, all else being equal. This will support the cyclical recovery across EM, albeit to various degrees. In addition to highly stimulative fiscal policy in developed markets (“DM”), we also expect the systemic CBs to remain flexible, patient and react only to sustained higher (average) inflation. Against this backdrop, we do not anticipate global financial conditions to tighten to a level that challenges the global recovery in the near term, but select EM economies more vulnerable to outflows may face greater pressure to adjust policy more swiftly, potentially shortening their cyclical rebound.  However, our analysis points to better resiliency in terms of EM fundamentals and technicals vs. the time of the so-called “taper tantrum” back in 2013. As such, many emerging market economies seem to be better positioned now to navigate a more turbulent market environment in the event of escalating concerns about potential Fed tapering in 2022 and beyond.

However, our analysis points to better resiliency in terms of EM fundamentals and technicals vs. the time of the so-called “taper tantrum” back in 2013. As such, many emerging market economies seem to be better positioned now to navigate a more turbulent market environment in the event of escalating concerns about potential Fed tapering in 2022 and beyond.

As the vaccine story plays out in the developed world through the remainder of 1H21, growth momentum is likely to continue to outperform while higher real yields in the U.S. erode interest rate differentials relative to EM. However, swift policy action or market repricing in select markets with light positioning will likely create attractive opportunities throughout the quarter.

As the vaccine story plays out in the developed world through the remainder of 1H21, growth momentum is likely to continue to outperform while higher real yields in the U.S. erode interest rate differentials relative to EM. However, swift policy action or market repricing in select markets with light positioning will likely create attractive opportunities throughout the quarter.

In 2021, although we have witnessed higher interest rates, we continue to believe that: (1) rates will remain at historically low levels, and (2) central bank balance sheets will keep growing. Thus far, higher yields have not catalyzed outflows from EMD similar to what the market witnessed during the Taper Tantrum or other rising rate environments. Fiscal stimulus has been and will continue to be made available in the U.S. and EM/DM. As all this money sloshes around, public market asset prices should continue to inflate. Subject to a change in current COVID-19 vaccine projections or unforeseen geopolitical events, we continue to believe 2021 should be a good year for risk markets. Nonetheless, we expect continued bouts of volatility that will provide dynamic asset allocation opportunities in both absolute and relative value. As such, we will continue to employ our barbell approach of anchoring our multi-asset portfolios with high conviction public credit and private credit on one side and dynamically asset allocating to dislocations, opportunistic credit and special situations on the other side.

COVID-19 vaccine roll-out in the U.S. in the first quarter has been in line with expectations. We believe second quarter vaccine supply and roll-out will exceed projections made at the beginning of 2021. Absent a wide-spread variant outbreak in the U.S., the U.S. will begin to emerge from COVID-19 in late Q2 and early Q3 and economic growth will significantly tick up.

As we heard last week from Chair Powell, the Fed is committed to a loose monetary policy through 2023. Absent a change in Fed leadership, we see low risk that they back down from this accommodative policy, as in doing so, they would lose tremendous credibility and risk unhinging the markets. The risk of this policy continuity is being proven wrong through their high conviction that higher prices will not evolve into an unexpected inflationary trend that forces the Fed’s hand prior to 2023.

That being said, we believe that material concerns over inflation in the bond market are not warranted. The U.S. has not witnessed material inflation since the early 1980’s. Globalization, technology, retail consolidation and worldwide demographics still favor deflation. There could be some supply and demand factors that contribute to higher prices with (1) de-globalization as it pertains to China and (2) peak U.S. millennial household formation. However, we suspect a lot of China production will be replaced by similarly priced EM production and there are not enough U.S. millennials to offset declining demand from other population segments in the DM world. The Fed also has the comfort of knowing that, if the increase in the money supply triggers unwanted inflation, it has all the ammunition it needs to address it with rate hikes from zero and the tapering of asset purchases (or, even more dramatically, by leaking balance sheet). Our guess is that prices tick-up slightly in the next few quarters in response to the stimulus bill and potentially an infrastructure bill but, absent congressional spending beyond that, 2H 2022 inflation will not exceed the Fed’s guidance. As such, market dips premised on inflationary fears will provide buying and portfolio rotation opportunities.

Geopolitically, although the U.S. is signaling more internationalism, we still see a high probability that the economic decoupling between China and the U.S. continues. President Biden does not appear to be reversing any of the Trump era policies (e.g. tariffs). Investors must keep an eye out for any escalation that would create global volatility.

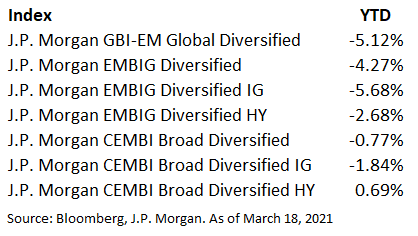

EM Debt has fared relatively well in 1Q considering the sizable move in U.S. Treasury yields with 10yr bonds wider by 77bps and the 2-10 curve steeper by 74bps but dispersion between return streams is quite high. As we expected, and in-line with our positioning, High Yield (“HY”) outperformed Investment Grade (“IG”) and Corporates outperformed Sovereigns (Hard and Local Currency).

We believe the better performance of EM Debt compared to other episodes of significantly higher U.S. Treasury yields in a short period of time comes down to a combination of better growth/results than initially feared, attractive relative valuations and continued solid technicals.

We believe the better performance of EM Debt compared to other episodes of significantly higher U.S. Treasury yields in a short period of time comes down to a combination of better growth/results than initially feared, attractive relative valuations and continued solid technicals.

While we have witnessed high dispersion, growth has generally been better than feared, supported by economic recovery and higher commodity prices for exporters. EM Corporate fundamentals overall proved to be resilient in 2020 with only a slight increase in net leverage of 0.2x and 0.3x for EM Corporate IG and HY, respectively. EM IG Corporate net leverage remains about a turn lower versus for U.S. credits while the HY differential has widened materially to 1.7x as EM HY Corporate kept more cash on their balance sheets to shield themselves from macro headwinds. We expect EM Corporate default rates to remain low as in 2020 as EM Corporate fundamentals overall have proven to be resilient and the external financing environment remains open and healthy for EM Corporates.

Accordng to EPFR, at mid-March, EM Debt inflows stand at $6.7bn in 2021, after inflows of $12.6bn in 2020. The $3.5bn outflow cycle associated with U.S. Treasury volatility in February/March is expected to reverse as markets normalize and EM spreads remain attractive on a relative basis. To that point, inflows into Local Currency funds have remained robust, up $12.9bn in 2021 and 3x larger than the flows seen in 2020.

Valuations in HY look compelling with spreads still about 100bps from the 2018 tights in Corporates and about 200bps in Sovereigns, respectively. This leaves us with a healthy spread buffer to counter higher interest rates if and when U.S. Treasury yields stabilize.

As the Fed failed to fully re-assure markets at March’s FOMC, we believe rates may remain under pressure in the short-term. As such, we do not believe it is time to add to allocations just yet. However, we are not too far from an attractive entry point (either side of 10yrs at 2pct) and believe that reduced volatility due to stability at higher levels will likely lead to pronounced credit spread tightening, especially for those credits that have a sizable spread buffer (mainly HY) and local markets with attractive FX. In our Corporate and Sovereign Strategies, this would lead to an increase in beta via High Yield and duration whereas in our Blended Strategies, we would aim to rotate from our sizable overweight in Corporates to Sovereigns (mainly HY in hard currency) and local markets with attractive FX.

Lastly, we have launched our enhanced “ESG 2.0” process for both Sovereigns and Corporates. Rather than simply using ESG as a portfolio filter, we are actively incorporating ESG into our investment process via security selection, conversations and terms with issuers. Further, we are seeking ESG oriented alpha by assigning granular ESG scores and forecasting the direction of those scores. This process aims to identify ESG rising stars and fallen angels similar to the way we have for many years relative to investment ratings.

Within Capital Solutions/Private Credit, from a bottom-up angle we see activity picking up as borrowers as well as market participants are starting to have more mobility. Diligence meetings and underwriting processes are getting back to normal. Furthermore, as we see an increase in volatility in the public markets which makes the primary issuance of public instruments more difficult, mid-size borrowers tend to focus and rely more on private credit. From a top-down approach, we’re monitoring the macro impact of COVID-19 in different countries and while we see that the vaccination phase is uneven across different regions and countries, it has not been a major impediment to the companies in the sectors that we have been focusing on, namely: trade finance, infrastructure and energy projects which continue to present good opportunities. In the case of trade finance and working capital financing, we could see additional flow as the filing of Greensill could leave some borrowers without access to credit. What we like about our financings is that we incorporate “back to basic” structures that provide unique downside protection to take advantage of this important asset class.

In our Opportunistic Credit Strategies, we will continue to dynamically shift between high yield, dislocated and distressed opportunities. In the first quarter, we were able to materially outperform and buffer the beta drag with opportunistic hedges, security selection and active rotations.

In Argentina, we continue to believe they are on-track for an Extended Fund Facility with the IMF but we are frustrated to see them potentially delaying the timing due to better local financial conditions (less pressure) and posturing for the upcoming mid-term elections. Nonetheless, we do anticipate an IMF deal later this year and expect that ratings upgrades to single B and extreme cheapness to comparable credits will provide for lower yields/higher prices.

In Special Situations, we have been actively working through our hurricane related insurance claims. While doing so, we see continued investment opportunities in litigation finance, particularly in international arbitration related to EM countries and insurance claims that we are underwriting.

In conclusion, despite certain risks and uneven initial conditions, we believe the balance of 2021 will prove to be a strong period for both economic and financial market performance in certain EM markets and assets. We intend to continue to lean-in and participate in both public and private EM credit markets as well as in special situations. However, we will do so consistent with the global top-down themes that we have identified. We will be keen to differentiate between winners and losers and dynamically asset allocate as absolute and relative value changes. This will entail constant triage of both top-down and bottom-up factors that will inform our dynamic asset position/allocation, planning the trade/trading the plan and agile hedging.