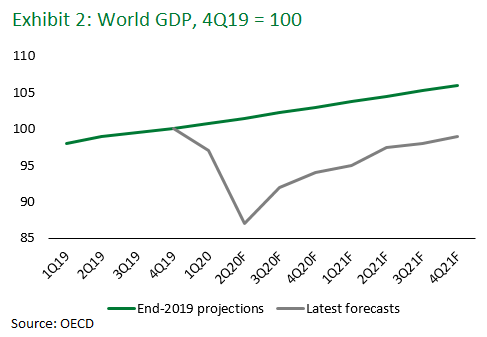

With the ongoing surge in COVID-19 cases across most of the Northern Hemisphere, including in the U.S. and Euro Area, the global economic recovery is poised to lose momentum in 1Q21, with a number of high frequency and mobility indicators pointing in that direction. However, the outlook for the whole of 2021 is supported by the prospect of rapid normalization from 2Q onwards as warmer weather arrives in the large developed economies and multiple, highly effective vaccines are deployed to an increasingly larger segment of the world’s population. In the meantime, global policy support, both monetary and fiscal, remains of paramount importance to bridge economies, companies and consumers to the “light at the end of the tunnel” provided by the expected start of a journey toward global herd immunity through vaccination.

With the ongoing surge in COVID-19 cases across most of the Northern Hemisphere, including in the U.S. and Euro Area, the global economic recovery is poised to lose momentum in 1Q21, with a number of high frequency and mobility indicators pointing in that direction. However, the outlook for the whole of 2021 is supported by the prospect of rapid normalization from 2Q onwards as warmer weather arrives in the large developed economies and multiple, highly effective vaccines are deployed to an increasingly larger segment of the world’s population. In the meantime, global policy support, both monetary and fiscal, remains of paramount importance to bridge economies, companies and consumers to the “light at the end of the tunnel” provided by the expected start of a journey toward global herd immunity through vaccination.

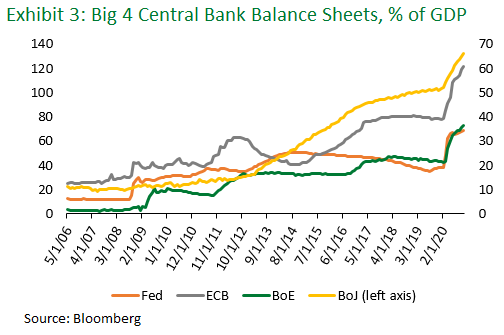

A gradual and incomplete global economic recovery is not great news over the medium-term, but for markets in the context of 2021, it comes with a critically important silver lining. We expect the global “liquidity wave” relentlessly provided by the systemically important central banks (Exhibit 3) to remain the most important factor supporting risk markets, including emerging markets (“EM”) .

.

Another important implication of the gradual and partial economic recovery relative to the pre-crisis trajectory (that was already relatively lackluster) is that inflationary pressure in the global economy in general, and the key

developed markets in particular, should remain muted, despite the likely increase in fiscal stimulus. This gives us comfort that developed market (“DM”) monetary policy is unlikely to change materially in the near-term,

maintaining unprecedented level of accommodation for the foreseeable future.

We believe that the market tailwind of extremely accommodative global monetary policy will not be derailed by the “Blue Wave” scenario that transpired in the US after the recent Senate runoff races in the state of Georgia gave the Democrats full government control over the next two years. In our view, EM will benefit from a shift back to multilateralism and gradual global trade normalization under President Biden in addition to positive spillover effects from likely further sizable fiscal stimulus (to the tune of $750bn-1trn) in the early days of the incoming administration. At the same time, although more fiscal stimulus by a unified Democratic government is likely to prove reflationary this year, we do not expect U.S. interest rates to increase to a level that would challenge our tactically constructive EM outlook.

Until sustained higher inflation materializes, which is unlikely in the near-term, the systemic central banks are set to continue pumping additional liquidity into the global system. To put things in some numerical context, the top eight DM central banks are expected to add liquidity of between 0.5% and 1.0% of their economies’ annual nominal GDP, on average, every month in 2021. In addition to new QE liquidity, we believe that substantial existing liquidity on the sidelines is likely to be increasingly invested and find its way into EM in 2021 as the arrival of effective vaccines helps investors see the light at the end of the COVID-19 tunnel.

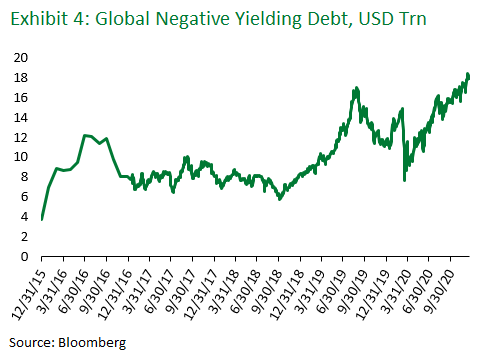

Importantly, new and existing liquidity will continue to be deployed in a context where yield is hard to find. Due to financial repression by the DM central banks, around $18 trillion of bonds trade with negative nominal yields (Exhibit 4) and about 75% of DM sovereign debt trades at negative real yields. This is set to continue to benefit EM assets, in both hard and local currency, amid what we expect to be a “search for yield” environment next year.

Importantly, new and existing liquidity will continue to be deployed in a context where yield is hard to find. Due to financial repression by the DM central banks, around $18 trillion of bonds trade with negative nominal yields (Exhibit 4) and about 75% of DM sovereign debt trades at negative real yields. This is set to continue to benefit EM assets, in both hard and local currency, amid what we expect to be a “search for yield” environment next year.

In 2021, we believe that: (1) rates will remain at historically low levels, and (2) central bank balance sheets will keep growing. There is no change in Fed leadership and Yellen (as a known commodity) is unlikely to deviate much on policy. Fiscal stimulus will continue to be made available in the U.S. and EM/DM. The only question is sizing, duration and effectiveness. As a result of the foregoing, public market asset prices should continue to inflate. Subject to a change in current COVID-19 vaccine projections or unforeseen geo-political events, we believe 2021 should be a really good year for risk markets.

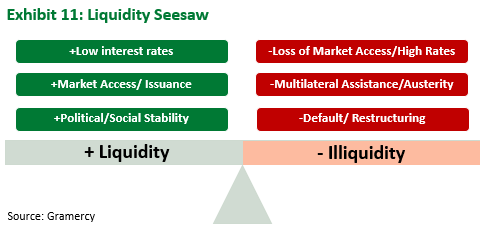

We expect that as long as liquidity remains robust, sovereign and corporate issuers will continue to have access to primary markets. If/when we experience bouts of illiquidity or a permanent reversal of liquidity conditions, then primary markets will become tighter and more selective. The resulting impaired market access may force some sovereign issuers to seek multilateral assistance and impose the burden sharing (restructurings) that would accompany such programs. Similarly on the corporate side, lack of liquidity/primary markets could also lead to restructurings and bankruptcies (See Exhibit 11).

On the COVID-19 front, our view is that the more aggressive “UK strain” is a red herring – any increase in short-term transmission rates will not have long-term consequences beyond further exascerbating what will already be a difficult winter for the UK and any other jurisdiction that potentially experiences this strain. However, now the light at the end of the tunnel is no longer a train but a vaccine(s). All that really matters is their effectiveness and the speed of “roll-out” as we march toward some sort of herd immunity. We will return to the “new, new normal” by the end of this summer as office workers will begin to return in mass to their “hybrid” offices just after Labor Day. In sum, 2021 should be a tale of two halves; the first half hindered by the residual challenges, damages and scarring of the COVID-19 crisis followed by the roaring 2020’s characterized by herd immunity/effective vaccines, the release of pent-up demand and a sharp economic rebound.

On the COVID-19 front, our view is that the more aggressive “UK strain” is a red herring – any increase in short-term transmission rates will not have long-term consequences beyond further exascerbating what will already be a difficult winter for the UK and any other jurisdiction that potentially experiences this strain. However, now the light at the end of the tunnel is no longer a train but a vaccine(s). All that really matters is their effectiveness and the speed of “roll-out” as we march toward some sort of herd immunity. We will return to the “new, new normal” by the end of this summer as office workers will begin to return in mass to their “hybrid” offices just after Labor Day. In sum, 2021 should be a tale of two halves; the first half hindered by the residual challenges, damages and scarring of the COVID-19 crisis followed by the roaring 2020’s characterized by herd immunity/effective vaccines, the release of pent-up demand and a sharp economic rebound.

Geopolitically, we see a high probability that the economic decoupling between China and the U.S. continues. While Biden is surrounded by advisers that are perceived as China friendly (i.e. Blinkin and Sullivan), recent history and Trump policies have successfully changed U.S. public opinion and policy and many global supply chains. This increases the overall business risk of reversing certain supply chains back into China (i.e. if Trump or someone like him can get elected in 2024, why reverse back into China from elsewhere in Southeast Asia even if Biden does lift sanctions just to take risk of re-reversing four years from now). While Biden may be lobbied by U.S. multinationals and Wall Street for a more relaxed China policy, he will not have much domestic political room to reverse many of the Trump era policies (e.g. tariffs) and we believe the U.S. national security apparatus is becoming more China hawkish. The economic concerns informing U.S.-China relations are quickly morphing into more permanent national security issues. The next phase of globalization will likely be driven by establishing a local presence to operate and sell locally rather than merely serving as a supply chain outpost.

So what does all this mean for Emerging Markets? More robust economic activity is good for EM, although growth will be uneven, delineating winners and losers. Stimulus and financial repression are here to stay, combining to be supportive with high demand for yield in both public and private EM credit. That being said, credit differentiation, specialization and the ability to underwrite and structure tailor made credit with adequate credit protections and uncorrelated collateral will prove to be key in navigating the K-shaped recovery.

The digital economy is here to stay as well, but not everything will be digital. We will seek both traditional (airlines, tourism, etc.) and non-traditional (Fintech, online retail, digital infrastructure) opportunities in EM. We expect a weak USD and continued oil price recovery, both of which should be supportive for EM in 2021. However, we wonder if and when we will witness the last hurrah for oil and gas as alternative and renewable energy sources begin to take over. We are on the lookout for when fossil fuels will become the Blackberry of energy. Relatedly, ESG as a material driver for EM investments, is as obvious today as globalization was 30 years ago.

In a world of structurally lower rates for longer, Emerging Markets Debt in hard-currency, especially in U.S. Dollar, is attractive on a relative basis. It remains one of the last scalable sources of yield for institutional investors that require robust investment returns to bridge the gap between their assets and liabilities without significant incremental risk. Indeed, Emerging Markets Debt’s consistently-better Sharpe Ratio compared to developed markets fixed income asset classes (namely, U.S. Investment Grade and High Yield), has, in Gramercy’s opinion, earned it a place as a core strategic allocation for institutional investors. Yet, this is not an asset class that is suitable for index funds. The need for active management is even more important in the difficult macroeconomic backdrop in which we find ourselves today, with a global pandemic going into second and third waves across the world that may have long-lasting consequences on global GDP, globalization and debt repayment behavior.

Despite the Emerging Markets Debt universe in hard-currency being a primarily an investment grade asset class, there will be significant headwinds to navigate. From a top-down perspective, next to the increasing importance of central bank policies and government stimulus, geopolitical risks as well as commodity markets, it is even more crucial to develop a deep understanding of valuations and technical drivers. A strong top-down framework will prove to be a key success factor in a world of detached valuations that are driven by technical factors more than macroeconomic and corporate fundamentals. However, while necessary, it will not be sufficient. Bottom-up factors will be as important, if not more, in certain circumstances. This is particularly true for granular analyses of creditworthiness, liquidity and other micro valuation metrics. Credit selection will be more critical than ever to avoiding unrecoverable mistakes and better managing downgrade risks. A deep pool of emerging markets investment professionals with experience through the credit cycle will be critical to successfully managing the increasingly difficult environment into 2021.

Investors seem to agree with our conclusions. As of December 2020, according to EFPR, inflows into Emerging Markets Debt in hard currency total $4.7bn and a stunning $24.4bn since April of 2020. In light of new lockdowns announced on a weekly basis, even a potential double-dip recession in much of the advanced world might not derail the investment case of Emerging Markets Debt in hard-currency so long as central banks response is timely. In fact, with highly effective vaccines being the light at the end of the tunnel, it might be a buying opportunity but one needs to know what to buy and manage it actively.

Within Private Credit, we see continued investment opportunities focused on trade finance, infrastructure and energy projects. From a geography perspective, we see a robust pipeline in Brazil, Mexico, Peru, Colombia, Turkey and Africa, especially for those companies that cannot access the capital markets but still want to take advantage of growth opportunities in their underlying businesses. We will continue to leverage our dedicated, local lending platforms to source, onboard, manage and monetize these credits.

In our Opportunistic Credit Strategies, we will continue to dynamically shift between high yield, dislocated and distressed opportunities. Ex-ante, we will use our distressed DNA to properly shield portfolios from defaults and bankruptcies and then ex-post to underwrite those situations whereby prices are materially below recovery values due to illiquidity/lack of index sponsorship (See Exhibit 12).

On a few specific names, in Venezuela, we believe that Biden will have more domestic political room to reverse tough Trump policies. The supporters of these policies primarily reside in South Florida, voted overwhelmingly Trump and are unlikely to swing Democrat anytime soon anyway. We believe that Biden will initially leave the sanctions in place as negotiating leverage and thereafter tone down the aggressive rhetoric with a softer approach. Current sanctions combined with the Biden approach/international diplomacy could be a very powerful combination for a political resolution in Venezuela that is planted in 2021 and harvested via internationally observed elections in 2022.

In Argentina, despite the political noise and volatility, pragmatism on all sides should deliver an Extended Fund Facility with the IMF by March or April. With Argentina yields 500-1000 basis points cheap to single-B rated comps, we believe the IMF agreement should catalyze materially lower yields/higher prices.

In Special Situations, we see continued investment opportunities in litigation finance, particularly in international arbitration related to EM countries. We also believe that we can continue to capitalize on insurance claims as its own asset class, both as a basis for litigation finance opportunities but also as a borrowing base for bespoke credit opportunities.

In conclusion, despite certain risks and uneven initial conditions, we believe 2021 will prove to be a strong year for both economic and financial market performance in certain EM markets and assets. We intend to lean-in and participate in both public and private EM credit markets as well as in special situations. However, we will do so in a disciplined, “happy trade” fashion whereby we scale-in over-time and will be happy to see markets rally and/or dip for further buying opportunities. We will also be keen to differentiate between winners and losers. This will entail constant triage of both top-down and bottom-up factors that will inform dynamic asset position/allocation, planning the trade/trading the plan and agile hedging.

In conclusion, despite certain risks and uneven initial conditions, we believe 2021 will prove to be a strong year for both economic and financial market performance in certain EM markets and assets. We intend to lean-in and participate in both public and private EM credit markets as well as in special situations. However, we will do so in a disciplined, “happy trade” fashion whereby we scale-in over-time and will be happy to see markets rally and/or dip for further buying opportunities. We will also be keen to differentiate between winners and losers. This will entail constant triage of both top-down and bottom-up factors that will inform dynamic asset position/allocation, planning the trade/trading the plan and agile hedging.

We thank everyone for their partnership and support in 2020. We wish you, your teams and your families a Happy and Healthy 2021.